Here is the most important truth in all of personal tax planning: most tax-saving opportunities disappear the moment the calendar flips to January 1.

Many tax-saving opportunities disappear once the calendar year ends. Reviewing your financial picture now allows you to maximise deductions, verify accuracy, and avoid stressful surprises during tax season.

This is not a minor observation. The difference between investors who act before December 31 and those who reflect on what they should have done in January is often measured in thousands of dollars — sometimes tens of thousands. And in 2026, with the One Big Beautiful Bill Act permanently reshaping tax brackets, contribution limits, charitable deduction rules, and estate exemptions, the year-end tax planning window has never been more consequential.

As the calendar approaches year-end, the One Big Beautiful Bill Act adds new layers to both current-year considerations and next-year planning, encouraging a fresh look at how income, deductions, and credits will be treated. Alongside the best practices that remain constant from one year to the next, this review can help you stay organised, take action before year-end, and begin 2027 on a strong financial footing.

Tax planning is not a once-a-year event — it is a continuous effort and a proactive collaboration between you, a financial advisor, and a tax professional to develop effective strategies that ensure tax compliance.

This complete year-end tax planning checklist gives you every action to take before December 31, 2026 — across retirement contributions, capital gains management, charitable giving, estate planning, and your complete financial planning review. Work through it now, with a qualified financial advisor, and enter 2027 with genuine financial confidence.

Why Year-End Tax Planning Is Worth Your Full Attention in 2026

The last quarter of the year is an ideal time to consider year-end tax planning strategies to potentially reduce taxes and help achieve long-term financial goals.

But the specific urgency of 2026 goes beyond the usual year-end calendar pressure. The extraordinary events of this year — a new Federal Reserve Chair eliminating forward guidance, CPI running at 4.2%, the S&P 500 delivering its worst single day of the year followed by continued record highs, the SpaceX IPO becoming the largest in financial history, and the Iran peace deal reshaping the energy and inflation outlook — have created a financial environment where the gap between investors with disciplined tax planning strategies and those without has never been wider.

Even if tax laws haven’t changed, your personal tax situation might look different than it used to — or vice versa. Your income, expenses, or deductions could have shifted, affecting your taxable income and adjusted gross income. Changes in your life, such as a new job increasing your ordinary income, additional investment income, or variations in expenses, can all have significant tax implications.

Let us work through every item on the checklist — systematically, completely, and with the specific 2026 context that makes each one more valuable than in any prior year.

✅ Section 1 — Retirement Account Contributions

Check 1 — Maximise Your 401(k) Contribution Before December 31

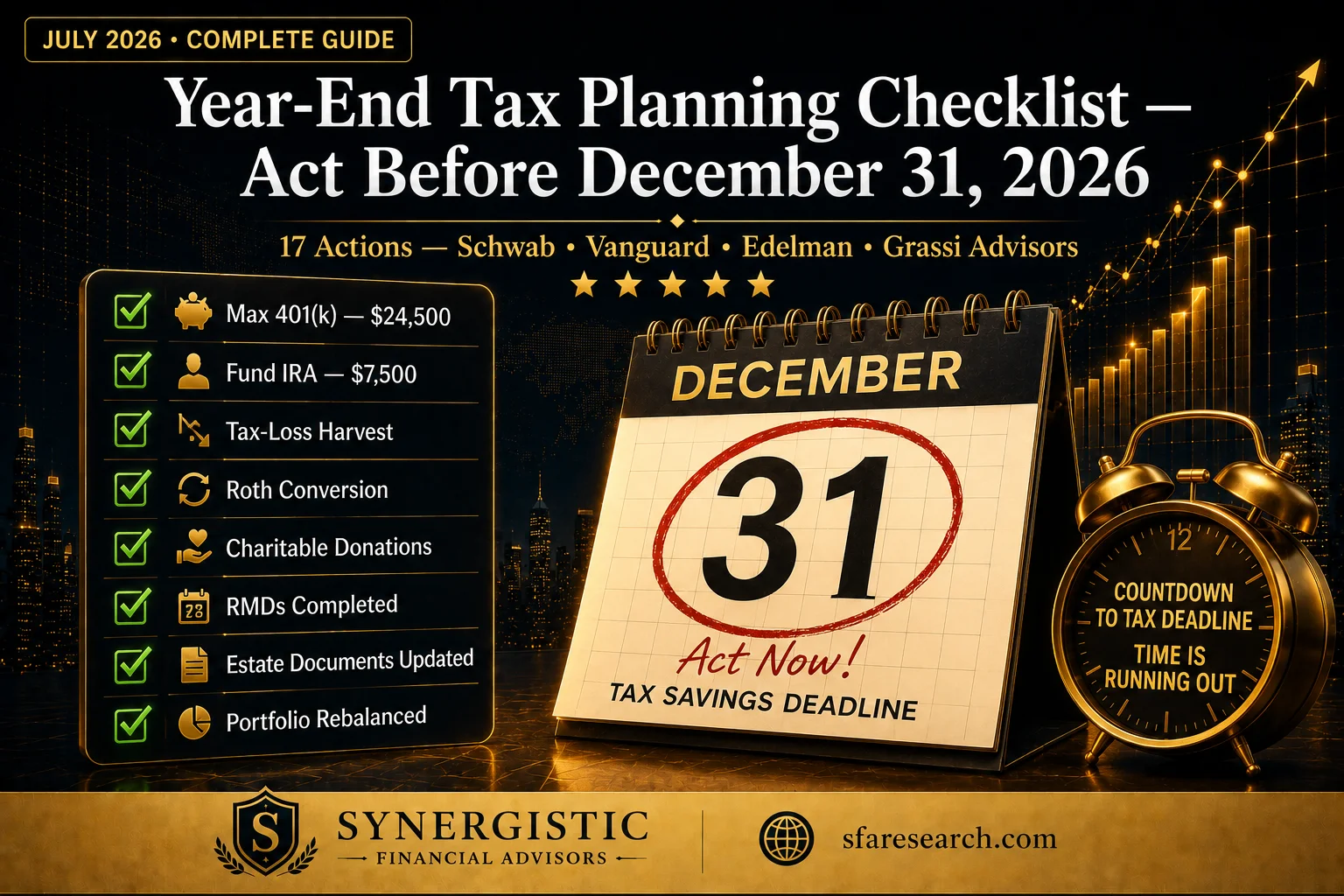

The IRS has confirmed that the 401(k) limit increases to $24,500 for 2026, and the IRA limit increases to $7,500.

Every dollar contributed to a traditional 401(k) reduces your taxable income dollar-for-dollar in the contribution year. If you have available payroll periods before December 31, increasing your contribution rate now — even modestly — can reduce your 2026 tax liability immediately. If you’re close to a tax bracket threshold, contributions may reduce taxable income into a lower bracket.

For those 50 and older, the catch-up contribution rules for 2026 deserve special attention. Catch-up contributions for those ages 50 or older are $7,500 for 401(k)s and $1,000 for IRAs. Beginning in 2026, catch-up contributions must be designated as Roth contributions if your 2025 wages were $145,000 or greater.

Individuals aged 60 to 63 can make the “super catch-up” contribution of $11,250 — for a total of $35,750 in 2026. If you fall in this age window, confirming with your plan administrator that super catch-up contributions are being captured before December 31 is one of the highest-value tax planning actions available to you this year.

Financial Planning Insight: A certified financial planner can model whether increasing your 401(k) contribution rate for your remaining 2026 payroll periods reduces your tax liability enough to justify the cash flow impact — and which account type (traditional vs Roth) delivers the optimal long-term after-tax outcome for your specific income and bracket situation.

Check 2 — Fund Your IRA Before the Deadline

While IRA contributions can technically be made until the tax filing deadline in April 2027 for the 2026 tax year, making your contribution before December 31 gives your investment an additional three to four months of tax-advantaged compounding. For Roth IRA contributions in particular — where every dollar grows permanently tax-free — that additional compounding window has meaningful long-term value.

Confirm you’ve fully funded retirement accounts — 401(k), IRA, HSA — and any self-employed retirement plans to benefit from tax deductions.

For self-employed individuals and business owners, the year-end retirement account deadline is even more consequential. SEP-IRA contributions for 2026 can be as high as 25% of compensation up to $70,000 — and must be funded by the extended tax filing deadline, not the calendar year-end. A financial advisor who coordinates your business and personal financial planning can help you determine the optimal contribution amount and structure before any deadline.

Check 3 — Maximise Your HSA Before December 31

Evaluating your retirement contributions to tax-advantaged accounts like your retirement plan or Health Savings Account can lower your taxable income.

The Health Savings Account remains the most underused triple-tax-advantage vehicle in the entire US tax code — with tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. For 2026, the HSA contribution limit is $4,400 for individual coverage and $8,750 for family coverage, with an additional $1,000 catch-up contribution for those 55 and older.

If you are enrolled in a high-deductible health plan and have not maxed your HSA contribution for 2026, this is one of the highest-return tax planning actions available before December 31 — delivering immediate tax savings while building a healthcare reserve that grows tax-free across your entire retirement planning timeline.

✅ Section 2 — Capital Gains and Investment Management

Check 4 — Review Your Portfolio for Tax-Loss Harvesting Opportunities

Review your portfolio to identify potential capital gains and losses. Tax-loss harvesting, which involves selling investments at a loss to offset gains elsewhere, can help manage taxable income. Don’t forget about the IRS wash sale rule, which prevents claiming a loss if you repurchase the same investment within 30 days.

2026 has delivered specific, measurable harvesting opportunities across the year — the June 9 selloff that pushed semiconductor stocks down 10% in a single session, oil volatility from $88 to $95 driven by the Iran peace deal timeline, and individual sector rotations that have left meaningful unrealised losses in some positions even as the overall market has climbed.

Any harvesting decisions should be considered with an investment advisor, accounting for the impact on long-term allocation, as well as the wash-sale rule, which disallows deductions for substantially identical securities purchased within 30 days before or after the sale.

Capital losses offset capital gains dollar-for-dollar. If your losses exceed your gains, up to $3,000 of the net loss can offset ordinary income annually, with any remaining losses carried forward indefinitely. Year-end is the optimal moment to systematically identify and capture these opportunities before December 31 closes the 2026 window.

Financial Planning Insight: A financial advisor who reviews your complete portfolio management positions — across every account — can identify specific harvesting opportunities that a position-by-position individual review consistently misses. The coordination across taxable accounts, retirement accounts, and different account types is where professional investment management adds the most measurable tax value.

Check 5 — Review Your Capital Gains Position for the Year

Review taxable accounts and consider tax-efficient strategies for gains, losses, and income from taxable investments.

If you have realised significant capital gains during 2026 — from the SpaceX IPO, from AI and technology position sales, from real estate transactions, or from business sales — December is the time to assess your total capital gains position and determine whether additional loss harvesting can meaningfully reduce your tax liability before year-end.

The long-term capital gains rates for 2026 remain at 0% for those with taxable income below $49,450 single or $98,900 joint, 15% up to $549,450 single or $600,050 joint, and 20% above those thresholds. If your income position allows for 0% rate gains harvesting — resetting cost basis on appreciated positions at zero federal tax cost — this is one of the highest-value year-end tax planning opportunities available.

Check 6 — Consider Your Roth Conversion Opportunity Before Year-End

Roth conversions: If taxable income is lower than expected this year, a Roth conversion may be a worthwhile strategy. This strategy transfers funds from a traditional IRA to a Roth IRA, paying tax at current rates in exchange for tax-free qualified withdrawals.

December is the final opportunity to execute a 2026 Roth conversion — and with the One Big Beautiful Bill Act having permanently established tax brackets, the planning certainty for multi-year Roth conversion strategies has never been higher. The optimal conversion amount depends on your specific income position, filing status, and bracket situation — a calculation that a certified financial planner can model precisely in your final December review.

The key consideration: converting the right amount fills your current tax bracket without pushing income into the next bracket, avoids triggering IRMAA Medicare surcharges, and maximises the tax-free growth opportunity while your tax liability on the conversion remains at the most favourable available rate.

✅ Section 3 — Charitable Giving Strategies

Check 7 — Make or Accelerate Charitable Contributions Before December 31

Gather donation receipts, including cash and non-cash contributions. If you’re close to itemising, consider bunching contributions into the current year.

Starting in 2026, individuals taking the standard deduction will be able to deduct up to $1,000 for single filers or $2,000 if filing jointly for cash contributions to public charities.

This is a genuinely new and important 2026 provision — for the first time, non-itemisers can claim a limited charitable deduction for cash donations. If you are taking the standard deduction and have not yet made your planned 2026 charitable contributions, ensuring those donations are completed and documented before December 31 is now more tax-valuable than in any prior year.

For itemisers with higher income, the “bunching” strategy — concentrating multiple years of charitable donations into a single year — can push total deductions meaningfully above the standard deduction threshold. Make contributions or establish a Donor-Advised Fund by year-end to receive immediate tax deductions while allowing time to select charities.

Check 8 — Execute Qualified Charitable Distributions if You Are 70½ or Older

If you’re over 73, ensure RMDs have been taken to avoid penalties. Consider using Qualified Charitable Distributions to reduce taxable income.

For retirees aged 70½ and older, QCDs allow up to $105,000 annually to be transferred directly from a traditional IRA to a qualified charity — satisfying RMD requirements without the transferred amount counting as taxable income. This is one of the most powerful combined tax planning and charitable giving strategies available, potentially reducing adjusted gross income enough to avoid IRMAA surcharges and reduce the taxability of Social Security benefits simultaneously.

The QCD must be completed before December 31 to count toward the 2026 tax year — making this a specific, time-sensitive year-end action for any retiree with charitable intentions and traditional IRA assets.

Check 9 — Donate Appreciated Securities Rather Than Cash

For investors with significant unrealised gains in taxable accounts, donating appreciated securities directly to charity — rather than selling them and donating cash — provides the full fair market value deduction while completely avoiding capital gains tax on the appreciation. This combined benefit makes security donation one of the most tax-efficient charitable strategies available in 2026’s market environment, where the S&P 500 has generated significant unrealised appreciation across many investor portfolios.

Financial Planning Insight: A financial advisor who coordinates your charitable giving strategy with your overall tax planning and investment management position can identify the specific securities most appropriate for direct donation — maximising your philanthropic impact and your tax efficiency simultaneously.

✅ Section 4 — Required Minimum Distributions

Check 10 — Confirm All RMDs Are Taken Before December 31

Individuals age 73 or older must take required minimum distributions before December 31.

The penalty for failing to take a required minimum distribution is severe — 25% of the amount that should have been withdrawn (reduced to 10% if corrected promptly). With this penalty applying to every dollar of the missed RMD, confirming that all 2026 RMDs have been completed before December 31 is a non-negotiable year-end checklist item for every investor 73 or older.

Action to consider: Review the tax implications of taking RMDs from inherited IRAs versus leaving the money in the IRA. Beneficiaries who inherit an account from someone who was already taking RMDs are now subject to the 10-year rule and must withdraw a minimum amount after inheriting the IRA.

For those who have inherited IRAs, the 10-year distribution rule under SECURE Act 2.0 has specific annual distribution requirements that must be tracked and fulfilled — creating a tax planning complexity that many beneficiaries are not yet aware of. A certified financial planner can map out the optimal RMD strategy across both your own retirement accounts and any inherited IRAs to minimise lifetime tax liability.

✅ Section 5 — Income and Withholding Review

Check 11 — Review Your Estimated Tax Payments and Withholding

Compare your year-to-date tax payments with projected liabilities. Adjust withholding to avoid underpayment penalties — or to prevent an unnecessary overpayment.

If you had a major life change — marriage, divorce, job change, or a new dependent — review your W-4 to ensure proper withholding.

In 2026, with CPI at 4.2% and the Federal Reserve projecting rates at 3.8% by year-end, investment income — from dividends, interest, and capital gains — has been meaningfully elevated for many investors. If your estimated tax payments have not kept pace with your actual income growth, you may be at risk of underpayment penalties. A year-end review of your total tax liability against payments made to date allows you to make an additional estimated payment before January 15, 2027 if needed.

Estimate your tax liability and adjust your withholding or estimated payments as needed. Use the IRS Tax Withholding Estimator to tailor your income tax withholding. Consult with a tax professional to explore tax-saving opportunities and tax-efficient investment strategies.

Check 12 — Review Your Income Timing Strategy

If you have control over the timing of income — through deferred compensation, business distributions, bonus timing, or freelance invoicing — December is the optimal month to assess whether accelerating income into 2026 or deferring it into 2027 produces a better overall tax outcome.

With 2026 brackets now permanent under the One Big Beautiful Bill Act, the calculation is more predictable than in previous years when legislative uncertainty clouded multi-year income timing decisions. A financial advisor coordinating with your CPA can model the precise after-tax impact of income timing decisions across both years.

✅ Section 6 — Estate Planning and Gifting

Check 13 — Use Your 2026 Annual Gift Tax Exclusion

The annual gift tax exclusion is $19,000 per donor per recipient in 2026 — meaning a married couple can gift $38,000 to each child, grandchild, or other recipient without any gift tax implications or use of the lifetime exemption. Gifts must be completed before December 31 to count toward the 2026 exclusion.

For families with meaningful estate planning objectives, the combination of the $19,000 annual exclusion with the permanently elevated estate exemption of $15 million per individual creates the most favourable multi-generational wealth management gifting environment in recent history. A financial advisor with estate planning expertise can help you build the annual gifting strategy that most effectively serves your long-term legacy intentions.

Check 14 — Review and Update Estate Documents

Review wills, trusts, and powers of attorney. Update beneficiaries and confirm titling on investment and bank accounts. Revisit your legacy and gifting plans to ensure alignment with your broader family goals.

Year-end is the optimal moment for an annual estate document review — ensuring that beneficiary designations, account titling, trust structures, and powers of attorney all reflect your current wishes and take full advantage of the 2026 legislative landscape. With the estate tax exemption now permanently at $15 million per individual, many estate plans built around the old $5-$12 million exemption levels need deliberate reassessment.

Ensure your will, trusts, and powers of attorney are current and reflect any life changes. Verify that all intended assets are properly titled in your trusts to avoid probate complications.

✅ Section 7 — Portfolio and Financial Plan Review

Check 15 — Rebalance Your Portfolio Before Year-End

Assess whether your portfolio aligns with your risk tolerance, time horizon, and goals. Rebalance to maintain your target asset mix, especially after a volatile year. Harvest losses strategically to offset capital gains where appropriate.

2026 has been one of the most extraordinary market years in recent memory — and extraordinary markets are precisely when portfolio management drift tends to be most significant. The AI and technology rally pushed large-cap growth positions to historically elevated weights. The semiconductor sector’s dramatic swings created concentration in some positions and losses in others. Oil volatility shifted energy sector weights. And the Iran peace deal changed the underlying assumptions for several sector allocations built earlier in the year.

A year-end portfolio management review — assessing actual allocations against target allocations and implementing systematic rebalancing — is one of the most consistently valuable investment management activities of the entire calendar year.

Check 16 — Review Your Insurance Coverage

Evaluate life, disability, and property insurance to ensure coverage aligns with your current wealth and family needs. If you’re approaching retirement, evaluate long-term care insurance options to protect against future healthcare costs.

Insurance needs often change as life evolves. Reviewing your policies annually helps protect against gaps.

Year-end is the right moment to confirm that your life insurance coverage reflects your current asset base and family obligations, that your disability insurance adequately protects your current income level, and that your property and liability insurance has kept pace with property value appreciation — which has been significant in most markets across 2025 and 2026.

Check 17 — Complete Your Comprehensive Year-End Financial Review

Year-end planning is more than a checklist — it is an opportunity to align today’s financial decisions with tomorrow’s goals. Whether you’re building wealth or focusing on preservation, these reviews can uncover opportunities for optimisation and peace of mind.

Year-end is the perfect time to showcase your value with clients from tax efficiency to long-term wealth building. Your insights, experiences, and personalised guidance can transform planning into progress — ensuring your clients’ strategy is not only sound but aligned with their values and goals.

A comprehensive year-end review with your financial advisor covers every dimension of your financial planning strategy simultaneously — investment management performance against goals, tax planning position at year-end, retirement planning projections updated for the year’s actual returns and new contribution rules, estate planning coordination, and your complete wealth management strategy for 2027 and beyond.

Tax planning is an ongoing collaboration between you, a financial advisor, and a tax professional. Meet at least annually to review your situation and make sure you’re exploring tax opportunities suited to your goals.

The Complete Year-End Tax Planning Checklist — At a Glance

| Category | Action | Deadline |

|---|---|---|

| Retirement | Max 401(k) — $24,500 ($32,500 if 50+) | Dec 31 via payroll |

| Retirement | Fund IRA — $7,500 ($8,600 if 50+) | April 2027 (but act now) |

| Retirement | Max HSA — $4,400/$8,750 | Dec 31 |

| Investments | Tax-loss harvesting | Dec 31 |

| Investments | Capital gains position review | Dec 31 |

| Investments | Roth conversion | Dec 31 |

| Charitable | Cash and security donations | Dec 31 |

| Charitable | Qualified Charitable Distributions (70½+) | Dec 31 |

| RMDs | Take all required RMDs (73+) | Dec 31 |

| Income | Review withholding and estimated payments | Dec 31 |

| Income | Income timing — accelerate or defer | Dec 31 |

| Estate | Annual gift exclusion — $19,000/recipient | Dec 31 |

| Estate | Review and update estate documents | Year-end |

| Portfolio | Rebalance to target allocation | Dec 31 |

| Insurance | Review all coverage | Year-end |

| Planning | Comprehensive financial review with advisor | Year-end |

The New 2026 Tax Rules That Change Your Year-End Checklist

Several provisions of the One Big Beautiful Bill Act create specific year-end opportunities and requirements that did not exist in prior years — and every investor’s year-end checklist must account for them.

Starting in 2026, individuals with FICA wages exceeding $150,000 will be required to make all catch-up contributions to the Roth 401(k). High-income savers over 50 must confirm their catch-up contributions are being directed to Roth accounts — not traditional — to maintain compliance with this new requirement.

Starting in 2026, individuals taking the standard deduction will be able to deduct up to $1,000 for single filers or $2,000 if filing jointly for cash contributions to public charities. This new above-the-line charitable deduction for non-itemisers is available only for 2026 and future years — making this the first year-end where this tax planning opportunity is actionable.

The SALT deduction cap temporarily rising to $40,400 in 2026 creates a specific year-end opportunity for high-income earners in high-tax states to review whether itemising now delivers greater savings than the standard deduction — and whether prepaying 2027 state and local taxes before December 31 captures additional 2026 deductions.

Why You Cannot Complete This Checklist Alone

The last few months of the year present some of the most valuable opportunities for year-end financial and tax planning. Once January arrives, many tax opportunities close until the following year. The time to prepare is now.

The 17-item checklist above is comprehensive — but its value depends entirely on the quality and coordination of its implementation. Harvesting the right losses while avoiding wash-sale violations requires coordination across your entire portfolio management structure. Determining the optimal Roth conversion amount requires modelling your complete income position, tax bracket, and IRMAA threshold simultaneously. Maximising charitable giving strategies requires coordinating account types, appreciation levels, and donor-advised fund timing. And managing RMDs across multiple inherited and personal accounts requires tracking that most individuals simply cannot maintain independently.

Look for a Certified Financial Planner or a fiduciary advisor. Ask for recommendations from friends, family, or colleagues. Check the advisor’s credentials and reputation.

A fiduciary financial advisor who works alongside your CPA — coordinating tax planning, investment management, retirement planning, and wealth management under one integrated advisory relationship — captures far more year-end value than any individual can working independently through a checklist. The coordination itself is where the most significant opportunities are found and the most costly mistakes are prevented.

How Synergistic Financial Advisors Executes Your Year-End Review

At Synergistic Financial Advisors, the year-end tax planning review is not an annual afterthought — it is the culmination of a year-round, proactive advisory relationship that has been monitoring opportunities and preparing strategies throughout 2026.

Our certified financial planner team works through every item on this checklist for every client — maximising retirement contributions across optimal account types, executing systematic tax-loss and gain harvesting across complete portfolio management structures, determining optimal Roth conversion amounts within precise bracket modelling, coordinating charitable giving strategies for maximum tax efficiency, confirming RMD compliance, reviewing estate documents and gifting strategies, and rebalancing every client’s portfolio management allocation against its year-end target.

We do this in coordination with your CPA — because the most powerful year-end tax planning happens when your financial advisor and tax professional are working from the same playbook simultaneously, with full visibility into your complete financial picture.

Meet with your wealth advisor to address any recent changes in your financial situation and discuss strategies for 2026. This is also a good time to discuss how upcoming tax law changes may impact your plans and identify proactive strategies for mitigation.

Ready to complete your year-end tax planning checklist with the guidance of a genuinely expert, fiduciary-standard financial advisor before December 31? Contact Synergistic Financial Advisors today.

👉 Visit sfaresearch.com — because the best tax planning happens before the deadline, not after it.

Final Thoughts — The Clock Is Ticking. Act Before December 31.

Proactive planning pays off. Reviewing financial statements, contributions, and documentation before the new year helps you avoid filing delays and missed opportunities.

The year-end tax planning checklist is not a bureaucratic exercise. Every item on it represents a genuine, time-limited opportunity to reduce your 2026 tax liability, improve your long-term retirement planning outcomes, and align your complete financial planning strategy with the specific opportunities that 2026’s legislative and market environment has created.

Most of these opportunities close permanently at midnight on December 31. The investors and business owners who work through this checklist deliberately, with expert financial advisor guidance, before that deadline will enter 2027 with a meaningfully stronger financial position than those who wait.

At Synergistic Financial Advisors, we help every client capture every year-end opportunity — through expert tax planning, disciplined investment management, comprehensive retirement planning, and complete wealth management coordination that leaves nothing on the table before December 31.