Here is the question that millions of people quietly ask themselves — usually at 11pm while staring at a financial decision they are not sure how to make: do I actually need a financial advisor?

The honest answer is that most people wait far too long. They wait until their finances feel overwhelming. They wait until they have made a costly mistake. They wait until they are already behind on retirement planning and realise the window for easy corrections has quietly closed. One of the best times to hire a financial advisor is when you are starting to feel like you have done everything you know how to do and are wondering if there are other things you should be doing — but the reality is that the most valuable advisory relationships begin before that moment of doubt, not after it.

In June 2026 — with CPI at 4.2%, the Federal Reserve eliminating forward guidance, markets at record highs after a historic SpaceX IPO, new permanent tax laws reshaping every financial decision, and the most complex wealth management environment in recent memory — the cost of navigating these decisions without expert guidance has never been higher.

This guide tells you exactly when to hire a financial advisor, what the 12 clearest signs are that the moment has arrived, and how to find the right one for your specific situation.

The Wrong Way to Think About This Decision

Before examining when to hire a financial advisor, it is worth addressing the most common misconception that prevents people from making this decision at the right time.

Most people assume that hiring a financial advisor is something you do after you have accumulated a certain amount of wealth. They imagine a threshold — $500,000, $1 million, some arbitrary number — at which professional financial planning suddenly becomes relevant. Net worth and money to invest are the absolutely wrong metrics to use when figuring out if you are ready for a financial advisor — in fact, they are wholly irrelevant. Household income, for those in their 30s and 40s, determines whether you are at a point to warrant bringing on a certified financial planner. Wikipedia

You do not necessarily need to have a significant amount of money to work with a financial advisor. In fact, getting good advice early in your savings journey might make it easier to meet financial goals.

The right question is not “do I have enough money to need an advisor?” It is “are the financial decisions I am facing significant enough that expert guidance would materially improve my outcomes?” In most cases, the answer to that second question becomes yes far earlier than most people realise.

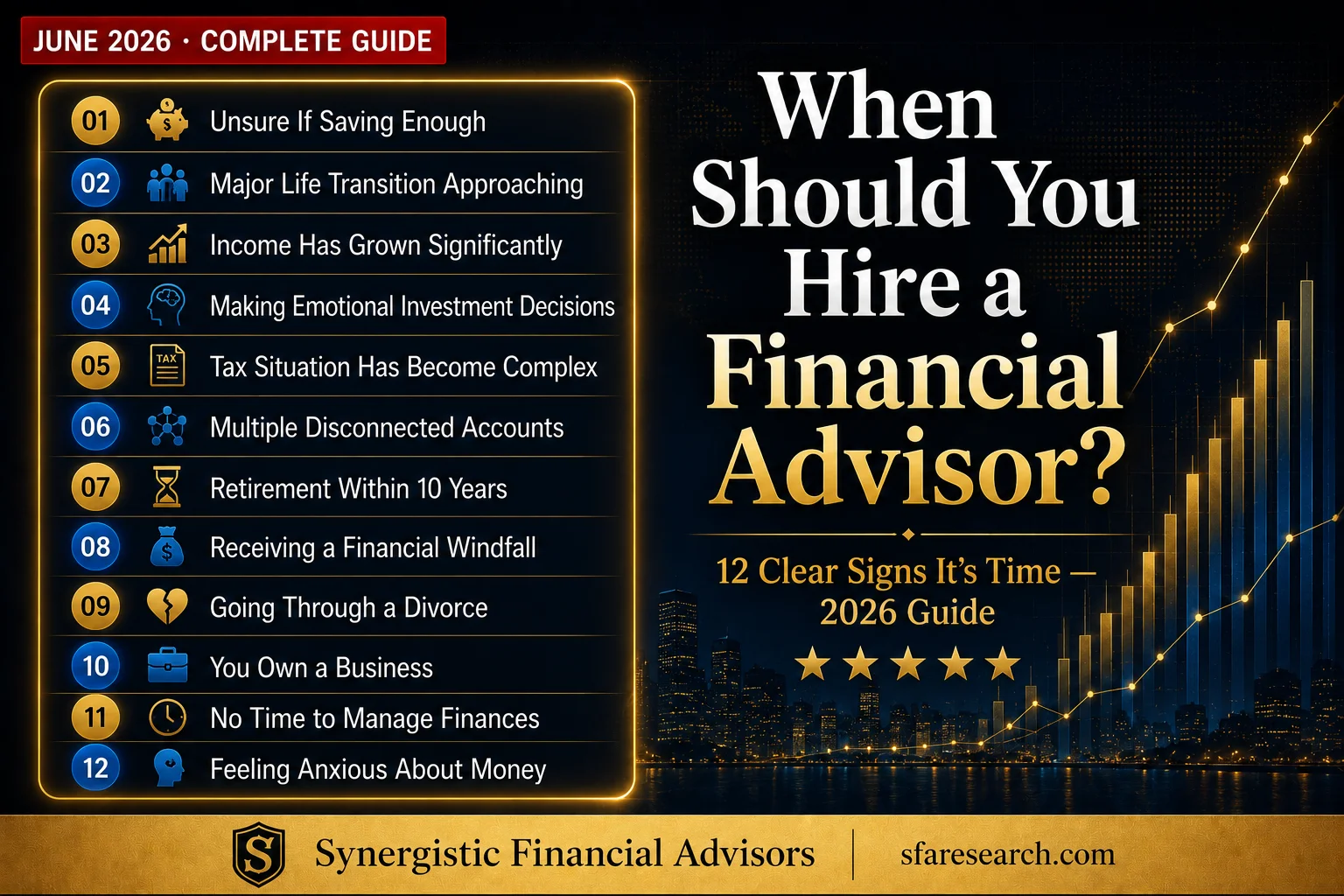

The 12 Clearest Signs It Is Time to Hire a Financial Advisor

Sign 1 — You Are Unsure Whether You Are Saving Enough

One of the earliest signs is uncertainty. If you cannot confidently answer how much you need for retirement planning, how long your savings will last, or whether your current strategy is on track, it may be time to bring in an expert. A financial advisor helps turn assumptions into numbers and clarity — assessing your income, savings, expected retirement age, inflation impact, and future expenses to build a realistic roadmap. Guesswork works early. Precision matters later.

In 2026, with CPI at 4.2% and the Federal Reserve now projecting rates at 3.8% by year-end, the gap between what people think they are saving and what they actually need has widened significantly. A certified financial planner can replace the anxiety of not knowing with a precise, data-grounded plan built around your actual numbers.

Sign 2 — You Are Approaching a Major Life Transition

Major milestones — such as marriage, childbirth, retirement planning, or inheriting a substantial estate — can radically change your financial picture. Knowing when to hire a financial advisor matters most during complex finances, major life events, or when planning for long-term goals. Acting proactively lets you optimise investments and create a cohesive financial plan that grows with you.

Life’s big moments — such as selling a business, receiving a windfall, or navigating an early retirement package — often carry significant financial implications. Missteps during these transitions can have long-lasting consequences. Financial advisors with experience in these scenarios can help you weigh options, understand potential outcomes, and align decisions with your broader financial goals.

The transitions that most commonly trigger the need for a financial advisor in 2026 include: getting married or divorced, having children, approaching retirement, receiving an inheritance, selling a business, receiving an equity compensation windfall from a technology company, or experiencing a significant income increase. Each of these events creates a planning opportunity that most people navigate less efficiently without professional guidance.

Sign 3 — Your Income Has Grown Significantly

A higher income brings opportunity but also complexity. Bonuses, business income, stock options, rental income, or multiple investment accounts require smarter coordination. Without proper planning, higher earnings can lead to higher taxes and inefficient investing. Hiring a financial advisor at this stage ensures your money works together instead of sitting in disconnected accounts.

This is one of the most consequential and most consistently ignored signs. As income grows, the tax planning complexity grows proportionally — and the gap between what you could be doing to optimise your situation and what you are actually doing tends to widen significantly without professional guidance. A financial advisor with genuine tax planning expertise can help high earners capture opportunities that generic financial advice completely misses.

Sign 4 — You Are Making Emotional Investment Decisions

There is no shortage of information out there when it comes to market analysis and predictions, but it can be difficult to determine just how much of this information represents real knowledge. Speaking with a financial advisor can help you see the signal through the noise and give you the confidence to stick to your investment management strategy even during periods of market volatility.

Market volatility can trigger costly behavioural mistakes, like selling investments during a downturn or buying near market tops. A financial advisor can coach you through short-term distractions to keep you focused on your long-term strategy.

June 2026 has tested this specific discipline repeatedly. The S&P 500’s worst single day of the year. The Fed eliminating forward guidance. The SpaceX IPO generating extraordinary excitement. Oil volatile between $88 and $95. Each of these events created genuine temptation to abandon disciplined portfolio management in favour of emotional reaction — and the investors who stayed disciplined were overwhelmingly those with qualified financial advisors keeping them grounded.

Sign 5 — Your Tax Situation Has Become Complex

If you are unsure how taxes will affect your retirement planning income, it is a strong signal that you should hire a financial advisor. Proper tax-aware planning can preserve more income over decades.

In 2026, the tax planning landscape has never been more consequential — or more complex. New permanent tax brackets under the One Big Beautiful Bill Act. A SALT deduction temporarily raised to $40,400. New catch-up contribution rules requiring high earners to direct contributions to Roth accounts. Estate exemptions at $15 million. Medicare IRMAA surcharges affecting high earners. And new senior deductions of $6,000 per person for those 65 and over.

Those who might benefit from hiring a financial advisor in 2026 include individuals unsure about retirement requirements, uncertain whether their portfolio management aligns with their goals, or uncomfortable managing finances independently.

A certified financial planner with integrated tax planning expertise can identify specific, measurable opportunities within this landscape that most individuals — however intelligent — will not find on their own.

Sign 6 — You Have Multiple Disconnected Accounts

Many people change jobs, move funds, or open different retirement accounts over time. Eventually, they lose track of how everything fits together. Multiple accounts without coordination often lead to overlapping investments, inconsistent risk exposure, and inefficiency. A financial advisor helps consolidate strategy without necessarily consolidating accounts. The goal is alignment, not complexity.

This is one of the most common situations that brings new clients to financial advisors — and one of the most immediately valuable problems professional financial planning solves. A fragmented financial picture — old 401(k)s from previous employers, multiple IRA accounts, taxable brokerage accounts, HSAs, and employer equity plans — creates invisible inefficiencies that compound silently into significant wealth erosion over time.

Sign 7 — You Are Planning for Retirement Within 10 Years

There is a reason that much of the financial advisory field focuses on retirement planning: preparing for and transitioning into this milestone phase involves every area of personal finance simultaneously — investment management, tax planning, Social Security strategy, healthcare planning, estate coordination, and wealth management all intersect in the decade before retirement.

As retirement begins to approach, this is a time when investors need to begin asking themselves a lot of difficult questions: What do you want to do with your time? How much will your retirement lifestyle cost? What are your fixed expenses? How will healthcare factor in?

A financial advisor who builds a comprehensive retirement planning strategy in the decade before your target date — optimising your Social Security timing, stress-testing your withdrawal strategy against multiple inflation and rate scenarios, building a healthcare cost reserve, and coordinating your tax planning across the transition — creates compounding value that dwarfs the advisory fees paid to access it.

Sign 8 — You Are Receiving a Financial Windfall

An inheritance, a business sale, an equity compensation vesting event, or a property sale can each create a sudden, significant increase in wealth that carries both extraordinary opportunity and genuine risk if managed without expert guidance.

Life’s big moments — such as selling a business, receiving a windfall, or navigating an early retirement package — often carry significant financial implications. Missteps during these transitions can have long-lasting consequences. Financial advisors with experience in these scenarios can help you weigh options, understand potential outcomes, and align decisions with your broader financial goals.

The tax planning decisions made in the first 12 months after receiving a significant financial windfall are often the most consequential financial decisions of a person’s life — and they are made under time pressure, emotional complexity, and with consequences that are very difficult to reverse. A fiduciary financial advisor provides exactly the objective, expert perspective that these moments demand.

Sign 9 — You Are Going Through a Divorce

Divorce is simultaneously one of the most emotionally demanding and financially consequential experiences in a person’s life — and one of the situations where professional financial planning guidance delivers the most measurable, tangible protection.

If money conversations are fraught with tension or avoided altogether, a financial advisor can be the perfect neutral third party — helping diffuse emotions and steer the conversation toward actionable feedback and concrete advice, serving as a sounding board and accountability partner through one of the most financially significant transitions in any individual’s life.

The wealth management decisions made during divorce — asset division, retirement account splitting, tax optimisation, insurance restructuring, and estate plan revision — each carry long-term financial consequences that a qualified financial advisor can help you navigate without the costly mistakes that emotionally driven decisions in high-stress transitions frequently produce.

Sign 10 — You Own a Business

Business ownership creates a unique financial complexity that most generic personal finance guidance is simply not designed to address. The intersection of personal and business finances — entity structure optimisation, qualified business income deduction, business-owner-specific retirement vehicles like SEP-IRAs and Solo 401(k)s, succession planning, key person insurance, and the eventual business exit strategy — requires a level of integrated financial planning expertise that makes professional guidance not optional but essential.

High-net-worth finances rarely exist in isolation. Investments, taxes, insurance, estate planning, and risk management all interact. A financial advisor can create an integrated approach so that every piece aligns with your broader objectives. By consolidating your financial picture, you gain clarity, control, and confidence in your decisions.

A financial advisor who understands both the personal and business dimensions of your financial life simultaneously is one of the most powerful assets any business owner can have.

Sign 11 — You Simply Do Not Have Time to Manage Your Finances Properly

Even if you have the skills to manage your finances, finding the time to stay on top of ever-changing tax laws, investment options, and financial strategies can be challenging. For busy professionals, entrepreneurs, and parents, this time investment often comes at the expense of other priorities like family or personal hobbies. Delaying critical financial decisions — such as estate planning or reallocating investments — can also be costly. A financial advisor can step in to handle these complexities, freeing up your time and ensuring timely decisions.

In 2026, staying current with financial planning best practices requires monitoring new tax legislation, Federal Reserve policy changes, market developments, portfolio management opportunities, and retirement planning rule changes — simultaneously. For individuals with demanding careers, businesses, or families, the time required to do this properly simply is not available. A financial advisor provides the expertise and the time investment that your financial future deserves, without requiring it to compete with everything else in your life.

Sign 12 — You Feel Anxious or Confused About Money

General signs that it might be a good time to call in the reinforcements include feeling stuck, overwhelmed, confused, or just a bit unsure if you are on the right track. Don’t wait until you are drowning in financial decisions to get help.

Financial anxiety is not a character flaw. It is information — and it is telling you that your current situation requires more expertise, more structure, or more guidance than you currently have access to. A qualified financial advisor replaces that anxiety with clarity, replacing vague worry with a specific, achievable, regularly reviewed plan that gives you genuine confidence in your financial future.

What Type of Financial Advisor Do You Actually Need?

Understanding when to hire a financial advisor is only half the equation — understanding which type is right for your situation is equally important.

Certified Financial Planner (CFP). The gold standard for comprehensive financial planning — covering investment management, tax planning, retirement planning, estate planning, insurance, and wealth management under one integrated framework. A certified financial planner is the right choice for most individuals seeking ongoing, comprehensive guidance.

Fiduciary Financial Advisor. A fiduciary financial advisor is legally required to act in your best interest at all times — without hidden commissions, without proprietary product pressure, and without conflicts of interest. This is the single most important quality to verify before engaging any financial advisor.

Independent Financial Advisor. An independent financial advisor operates without ties to any bank, insurance company, or investment firm — providing advice based purely on what is best for you rather than what generates the most revenue for a parent institution.

Investment Advisor. An investment advisor specialises specifically in investment management and portfolio management — appropriate for individuals whose primary need is portfolio construction and ongoing management rather than comprehensive financial planning.

Financial Planner. A financial planner focuses on building comprehensive long-term financial planning strategies — covering goals, budgeting, savings, retirement planning, and the complete financial roadmap that connects all of your financial decisions.

Financial Consultant. A financial consultant typically provides specific, project-based guidance — appropriate for individuals with a specific financial question or decision rather than a need for ongoing comprehensive advisory.

For most individuals in 2026, the combination of fiduciary status and the certified financial planner credential represents the baseline requirement for any advisory relationship worth entering.

How Much Does Hiring a Financial Advisor Cost in 2026?

Understanding the cost of professional financial advisory is essential — but it is equally important to understand the cost of not having one.

The cost of advisory services can be a significant factor. Financial advisors charge fees that may reduce your investment returns, especially if your assets are modest in value. Finding the right fit requires due diligence to find a trustworthy, competent advisor.

The most common fee structures in 2026 include AUM-based fees typically ranging from 0.5% to 1.5% of assets managed annually, flat annual retainer fees ranging from $2,000 to $10,000 or more depending on complexity, hourly fees typically between $150 and $400 per hour, and project-based fees for specific financial planning deliverables.

The critical perspective is not the absolute cost of advisory fees but the net value delivered. Research consistently shows that individuals working with qualified financial advisors achieve better long-term outcomes — through better investment management decisions, more efficient tax planning, optimal retirement planning timing, and the prevention of costly behavioural mistakes — than those who navigate these decisions alone. The value of professional guidance compounds over time in ways that advisory fees almost never outweigh for individuals with meaningful financial complexity.

The Question That Matters Most

The real question is not just when to hire a financial advisor — it is whether you are ready to invest in your financial future. Knowing when to hire a financial advisor is less about reaching a specific age or income level and more about recognising when financial decisions start carrying long-term consequences.

If you are reading this article, the answer to that question is probably yes. The fact that you are asking “when should I hire a financial advisor?” is itself one of the clearest signs that the moment has arrived.

How Synergistic Financial Advisors Serves Every Life Stage

At Synergistic Financial Advisors, we believe that genuinely great financial advisory does not begin at a specific wealth threshold or a specific age. It begins the moment your financial decisions start carrying meaningful long-term consequences — which is earlier than most people think, and almost certainly earlier than you have been told.

Our certified financial planner team provides genuinely comprehensive, fully integrated financial planning across every dimension of your financial life — from investment management and portfolio management to retirement planning, tax planning, estate coordination, and comprehensive wealth management — all delivered through an unwavering fiduciary commitment that puts your goals, your values, and your financial future above everything else.

Whether you are a young professional who wants to start building wealth intelligently from the beginning, a high-income earner navigating complex tax planning and equity compensation decisions, a business owner who needs coordinated personal and corporate financial planning, a family approaching retirement planning with both urgency and optimism, or someone searching for a financial advisor near me who genuinely understands your complete financial picture — Synergistic Financial Advisors is here to deliver the expert, personalised, fiduciary-standard guidance your financial future deserves.

Ready to stop wondering if you need a financial advisor and start experiencing what the right one actually does for your financial life? Contact Synergistic Financial Advisors today for a personalised consultation.

👉 Visit sfaresearch.com — because the best time to hire the right financial advisor is always now.

Final Thoughts — The Right Time Is Almost Always Sooner Than You Think

The 12 signs in this guide are not a checklist to complete before calling a financial advisor. They are indicators — any one of which, present in your life right now, makes professional financial planning guidance both appropriate and genuinely valuable.

Don’t wait until you are drowning in financial decisions to get help. The right financial advisor serves as a sounding board and accountability partner — someone to reach out to when you hit a roadblock, providing regular check-ins that keep you on track and motivated to reach your goals.

The investors, business owners, and families who look back on their financial lives with the greatest satisfaction are not those who waited until everything was perfectly aligned before seeking guidance. They are those who found the right financial advisor at the right moment — and built a financial future that reflected genuine expertise, genuine personalisation, and genuine care for what their money was actually for.

That financial advisor is waiting at Synergistic Financial Advisors.