Retirement planning is one of the most important financial decisions you’ll ever make. Yet many people entering their 30s, 40s, and even 50s still ask the same question: Should I invest in a 401(k) or an IRA?

The answer isn’t always straightforward. Both accounts offer valuable tax advantages and can help you build long-term wealth, but each comes with different rules, contribution limits, and investment flexibility.

If you’re looking for the best financial advisor for retirement planning and investment management, understanding the differences between a 401(k) and an IRA is a critical first step.

Understanding the Basics of 401(k) and IRA Accounts

A 401(k) is an employer-sponsored retirement plan that allows employees to contribute a portion of their salary before taxes. Many employers also offer matching contributions, which can significantly boost retirement savings.

An IRA (Individual Retirement Account), on the other hand, is opened independently and gives investors more control over investment choices.

Both accounts are designed to help individuals save for retirement while benefiting from tax advantages.

Key Differences Between a 401(k) and an IRA

Although both serve the same purpose, they differ in several important ways.

Contribution Limits

Generally, 401(k) plans allow significantly higher annual contributions than IRAs. This makes them attractive for individuals looking to maximize retirement savings.

Employer Matching

One of the biggest advantages of a 401(k) is employer matching. This is essentially free money that helps accelerate wealth accumulation.

Investment Options

IRAs often provide greater flexibility. Investors can choose from stocks, ETFs, bonds, mutual funds, and other assets.

Fees

Some employer-sponsored 401(k) plans have limited investment choices and higher fees. An IRA may provide access to lower-cost investment alternatives.

A professional financial advisor for retirement planning and portfolio management services can help determine which option aligns with your goals.

Which Account Offers Better Tax Benefits?

Tax advantages are one of the biggest reasons people invest through retirement accounts.

Traditional 401(k)

- Contributions are tax deductible.

- Taxes are paid upon withdrawal during retirement.

- Lower taxable income today.

Traditional IRA

- Contributions may be tax deductible.

- Investments grow tax deferred.

- Taxes apply when funds are withdrawn.

Roth IRA

- Contributions are made with after-tax dollars.

- Qualified withdrawals are tax free.

- Ideal for younger investors expecting higher future income.

Working with an independent financial advisor for tax planning and retirement strategy can help determine which tax approach best fits your situation.

Why Employer Matching Can Make a Huge Difference

If your company offers matching contributions, contributing enough to receive the full match is often one of the smartest financial decisions you can make.

For example:

Suppose you contribute 6% of your salary and your employer matches 6%.

That’s an immediate 100% return on your contribution before investment growth.

This is why many experts and the best financial advisor for financial planning and wealth management services recommend prioritizing employer matching before investing elsewhere.

When an IRA Might Be the Better Choice

An IRA may be more suitable if:

- You are self-employed.

- Your employer doesn’t offer a retirement plan.

- You want more investment flexibility.

- You prefer lower fees.

- You want access to individual stocks and ETFs.

Investors seeking customized portfolios often work with a financial planner near me for retirement planning and investment management strategy to maximize IRA benefits.

Can You Have Both a 401(k) and an IRA?

Yes.

In fact, many financial professionals recommend using both accounts.

This approach offers:

- Higher overall retirement savings.

- Additional tax advantages.

- Greater diversification.

- Increased investment flexibility.

Combining both accounts is often part of a comprehensive financial planning and wealth management strategy for long-term growth.

401(k) vs IRA for Different Age Groups

In Your 20s and 30s

Focus on growth. Roth IRAs are often attractive because future tax-free withdrawals can provide significant benefits.

In Your 40s

Maximize contributions and take advantage of employer matching.

In Your 50s and Beyond

Catch-up contributions become increasingly important. Balancing income needs and tax planning becomes essential.

Many people in this stage consult the best financial advisor near me for retirement planning and portfolio management services to optimize their savings.

Investment Flexibility: Which Wins?

IRAs generally provide greater investment choices.

Typical IRA investments include:

- Stocks

- ETFs

- Bonds

- Mutual funds

- REITs

Meanwhile, 401(k) plans usually offer a limited menu selected by the employer.

Investors who want greater control often prefer IRAs, while those seeking convenience may appreciate the simplicity of employer-sponsored plans.

Professional investment management services for long-term financial planning can help investors balance both approaches.

Common Retirement Planning Mistakes

Many people make mistakes that can reduce retirement income later.

Avoid these errors:

Ignoring Employer Matching

Failing to capture free matching contributions leaves money on the table.

Waiting Too Long

Starting early allows compound growth to work in your favor.

Not Diversifying

Holding too much in one asset class increases risk.

Ignoring Inflation

Inflation can significantly reduce purchasing power over decades.

Failing to Review Your Plan

Retirement strategies should evolve as life changes.

Working with an experienced financial advisor for retirement planning and investment management services helps investors avoid costly mistakes.

Which Is Better: 401(k) or IRA?

There is no universal answer.

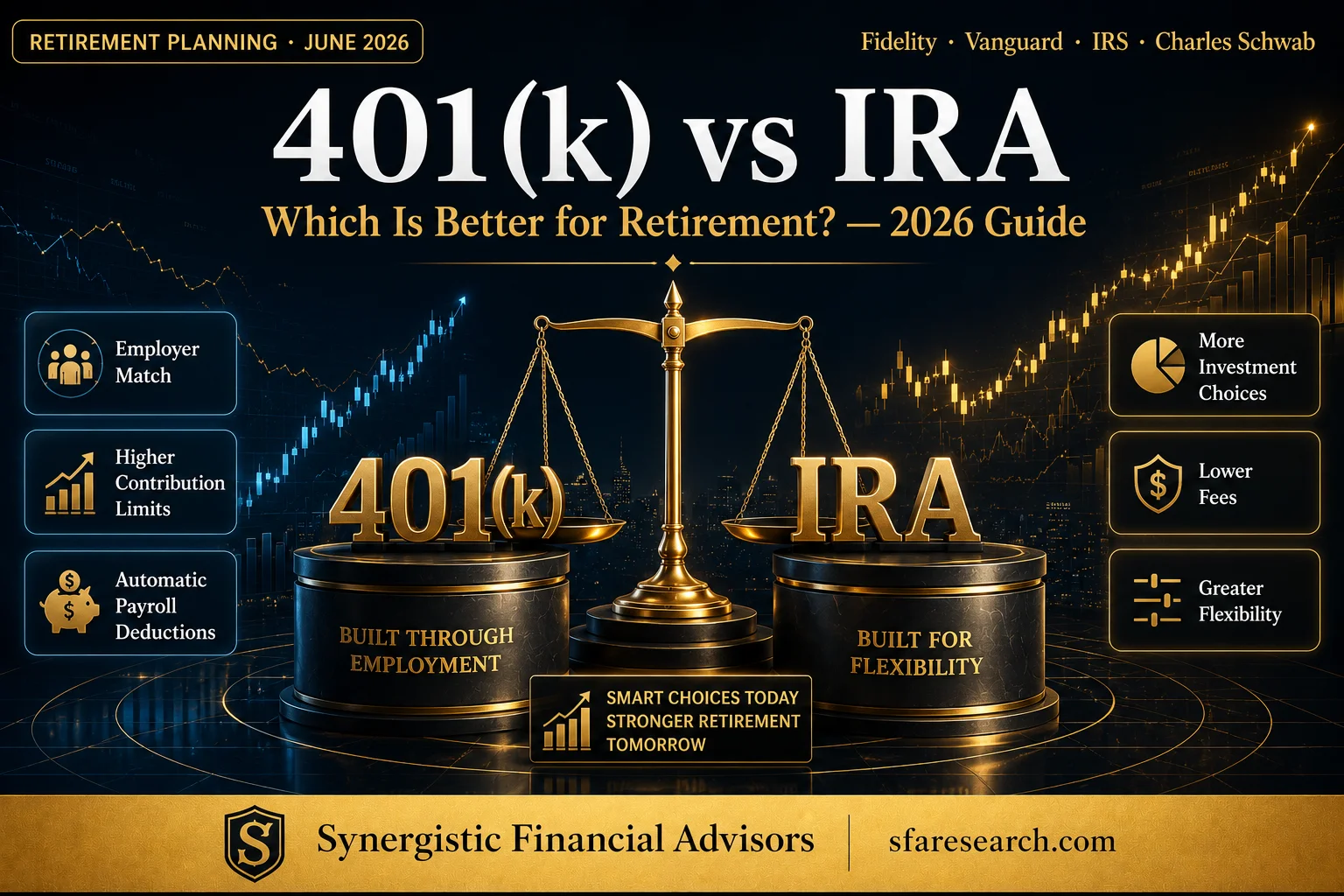

A 401(k) is usually better if:

- Your employer offers matching contributions.

- You want higher contribution limits.

- You prefer automatic payroll deductions.

An IRA may be better if:

- You want more investment options.

- You seek lower fees.

- You are self-employed.

- You want more control over your portfolio.

For many people, the best solution is using both.

The Role of Professional Financial Planning

Retirement planning goes far beyond choosing between a 401(k) and an IRA.

A comprehensive strategy includes:

- Tax planning

- Investment management

- Portfolio diversification

- Risk management

- Wealth preservation

Partnering with the best financial advisor for retirement planning and wealth management services can help ensure your retirement goals remain on track.

Final Thoughts

The debate between a 401(k) and an IRA isn’t about which account is universally better—it’s about which one fits your financial goals, income, and retirement timeline.

For many investors, combining both accounts creates a stronger foundation for long-term success.

With proper financial planning, professional investment management, and smart wealth management services, you can build a retirement strategy designed to provide financial independence and peace of mind.