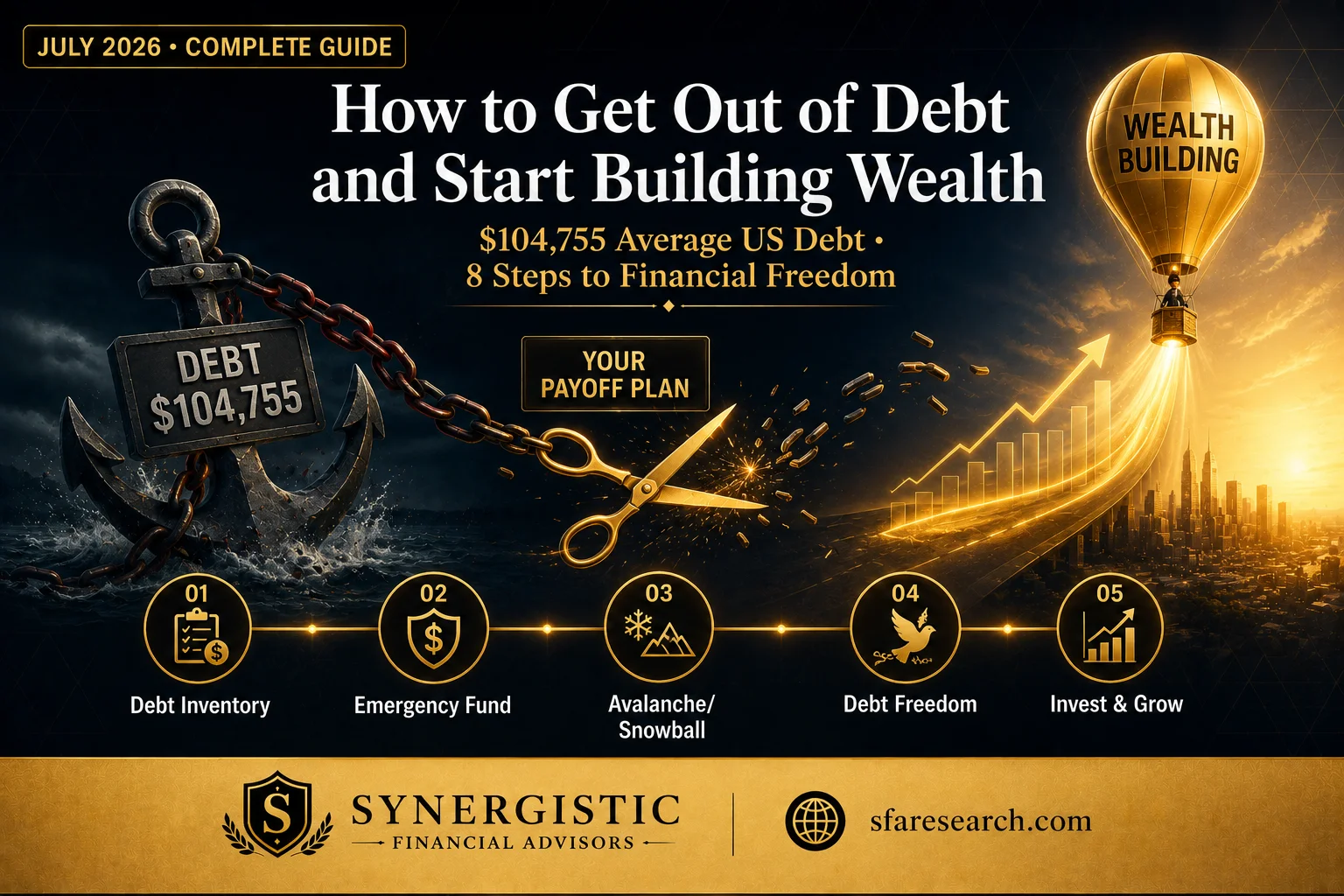

Here is the number that should stop you in your tracks: U.S. consumers carry an average debt balance of $104,755, according to Experian data from June 2025. Credit card balances alone — which tend to come with high interest rates — average $6,735 per person.

More than $104,000 in debt. For the average American family. Before a single investment decision, before a single retirement planning contribution, before a single step toward genuine wealth management — that is the financial reality most people are starting from in 2026.

But here is the truth that changes everything: getting out of debt is absolutely possible, regardless of your income. It takes a plan, discipline, and the right strategy for your situation.

And here is the insight that most debt guides never give you — getting out of debt is not the destination. Debt freedom is not the destination. It is the starting line for the most financially productive period of your life. Everything you build from that point forward is built on a foundation that is genuinely yours, with no portion already committed to servicing the cost of past decisions. That foundation changes everything.

Consider what becomes possible when the money that was going to credit card payments and loan installments every month is redirected into a diversified investment portfolio instead. Over a decade of consistent investing at that level, the compounding effect generates wealth that most people who have never been through a debt elimination journey find difficult to believe is achievable for someone of ordinary income.

This guide gives you the complete, data-backed, step-by-step framework for getting out of debt and building genuine, lasting wealth in 2026 — connecting the debt payoff journey directly to the investment management, retirement planning, tax planning, and wealth management strategy that follows it.

Step 1 — Understand Why You Are in Debt First

Before executing any strategy, the most important and most consistently skipped first step is honest self-assessment.

The first step is to understand “why you’re in debt in the first place.” “This is not a blame game,” said Kumiko Love, an accredited financial counselor. “This is simply understanding how you got here so you can set better management and healthy habits to maybe correct some of those things and or make different choices.”

Understanding the cause determines the cure. Medical debt requires a different response than lifestyle credit card debt. Student loan debt carries different strategic implications than high-interest consumer loans. A temporary income disruption creates a different debt profile than a pattern of chronic overspending.

Financial experts typically consider some debt “good” and some debt “bad.” Examples of good debt include most mortgages, business loans, and low-interest student loans. Good debt typically comes with a fixed payment schedule and may have a positive impact on your credit score, assuming you’re making on-time monthly payments. Bad debt is high-interest, typically the result of unpaid credit card bills or loans from predatory lenders.

This distinction matters enormously for strategy. Good debt — low-interest, tax-deductible, or value-generating — does not necessarily need to be eliminated before beginning to invest. Bad debt — high-interest credit cards, payday loans, high-APR personal loans — almost always should be eliminated before any serious investment management begins, because the guaranteed return of eliminating 22% credit card debt exceeds virtually every available investment return.

Financial Planning Insight: A financial advisor can help you map your debt landscape objectively — distinguishing between the debt that needs urgent elimination and the debt that can be managed alongside an emerging investment management strategy.

Step 2 — Complete Your Debt Inventory

You cannot fight what you cannot see. Before choosing any payoff strategy, you need a complete, honest picture of every debt you carry.

Creating an inventory of your current debts gives you a complete picture of where you stand and helps you identify the right payoff strategy. Create a list of all outstanding balances, including the creditor’s name, current balance, interest rate, monthly payment amount and due date, and other important details. Calculate your total debt load by adding up all the balances to fully understand how much you owe.

Calculate your totals: sum up your total principal balance across all debts and sum up your total minimum monthly payments. This gives you your baseline financial obligation. Understanding your interest rates is paramount. A credit card with a 24% APR isn’t just expensive — it’s a financial black hole.

The debt inventory serves three simultaneous purposes. It replaces vague anxiety with specific, knowable numbers. It reveals which debts are most expensive — costing you the most in interest each month and therefore warranting the most urgent attention. And it establishes the baseline against which you will measure your progress — which is one of the most powerful motivational tools available during what can be a long payoff journey.

Be completely honest with yourself during this step. Include every credit card, every personal loan, every medical bill, every student loan, every auto loan, and every other obligation. The debt you do not document is the debt that quietly continues compounding while you focus on the debts you do see.

Step 3 — Build Your $1,000 Emergency Fund First

This step seems counterintuitive — and it is the one that most debt guides either skip entirely or mention as an afterthought. But it is arguably the most important structural decision in your entire debt payoff journey.

Without an emergency fund, every unexpected expense — car repair, medical bill, broken appliance — goes straight onto a credit card, and your debt grows right back. Start small. Save $1,000 in a separate savings account before you go all-in on debt payoff. This mini emergency fund catches the most common surprises without derailing your progress.

For many people, the reason they keep returning to credit even while trying to pay it off is the absence of any financial cushion to handle unexpected expenses. When the car needs a repair or a medical bill arrives unexpectedly and there is no cash available, the credit card feels like the only option. Building even a modest emergency fund of one to two months of living expenses before you attack your debt aggressively gives you the buffer that prevents this cycle from repeating.

The $1,000 emergency fund is not a savings goal — it is a debt payoff tool. Without it, every unexpected expense re-opens the credit card wound you are trying to close. With it, the most common financial emergencies are absorbed by cash rather than credit — keeping your debt payoff trajectory on track through the inevitable surprises that life delivers.

Once your debt is eliminated, you will expand this emergency fund to the full three to six months of essential expenses that genuine financial security requires. But during the debt payoff phase, $1,000 to $2,000 in an accessible savings account is both achievable quickly and adequate to prevent the most common setbacks.

Step 4 — Choose Your Debt Payoff Strategy

With your debt inventory complete and your starter emergency fund in place, it is time to choose the core strategy that will drive your payoff. Two approaches dominate the research — and the right choice depends on your specific debt profile and your psychological wiring.

The Debt Avalanche — Maximum Mathematical Efficiency

The debt avalanche method saves the most money in interest. The approach is straightforward: the avalanche method involves paying more on the bill with the highest interest rate until it’s paid off, while still making minimum payments on your other debts.

The financial logic behind this approach is straightforward. High-interest debt costs you the most money for every day it remains outstanding. By eliminating the most expensive debt first, you reduce the total amount of interest that accumulates across your entire debt portfolio during the elimination period. Over the course of a multi-year payoff, this difference can be genuinely significant, amounting to thousands of dollars saved compared to paying debts in a different sequence.

The avalanche is the mathematically optimal strategy — and the right choice for people who are motivated by efficiency and who can maintain momentum knowing they are making the mathematically best possible decision even when visible progress feels slow.

The Debt Snowball — Psychological Power

The snowball method, popularised by “The Total Money Makeover” author Dave Ramsey, involves tackling your smallest debts first. Both methods require you to pay more toward one debt than others — but the snowball method can be motivating because it eliminates individual debts quicker.

The debt snowball method works best for motivation and early momentum. By achieving the psychological win of eliminating your first debt balance completely — however small — you build the confidence and momentum that sustains the longer journey of paying down larger obligations.

Which should you choose? The fastest approach depends on your situation. Combining a realistic budget with either the debt snowball or debt avalanche method is the strongest starting point. If you are highly analytical and motivated by efficiency, the avalanche typically saves more money. If you struggle with motivation and need early wins to stay committed, the snowball’s psychological benefits often produce better real-world outcomes — because the best debt payoff strategy is the one you actually stick to.

Step 5 — Attack Your Credit Card Debt With Urgency

High-interest debt should be the first kind you should tackle. “Credit card debt always is going to have a high interest rate. That’s probably the debt you need to work to eliminate first before you worry about your lesser interest debt,” said Dunlap.

The mathematics make this urgency undeniable. Credit card debt is the most expensive type of consumer debt, with average APRs above 20% in 2026. On a $5,000 credit card balance at 22% APR, making only minimum payments means you’ll pay over $7,000 in interest and take 20+ years to pay it off. Even an extra $50 per month cuts that timeline dramatically.

A $5,000 balance at 24% APR with a $100 minimum payment could take over 7 years to pay off, costing you nearly $4,000 in interest alone. Contrast this with a personal loan at 10% APR — the difference in cost and payoff speed is staggering.

Three specific tactics accelerate credit card payoff beyond minimum payments and raw extra payments.

Balance Transfer Cards: One way to consolidate debt is with a balance transfer to a credit card with a 0% APR introductory rate. While performing the balance transfer may come with a fee, doing this kind of debt consolidation effectively freezes your debt, so you won’t continue to accrue new interest. This is most effective for people with good credit scores who can realistically pay off the transferred balance within the 0% introductory period — typically 15-21 months.

Debt Consolidation Loans: The average credit card APR in 2026 is above 20%, while personal loan rates average around 12-13% for borrowers with fair to good credit. A consolidation loan that meaningfully reduces your interest rate — combined with a firm commitment not to rebuild credit card balances — can save thousands in interest and simplify your monthly payment structure.

Negotiating Directly With Creditors: Most major credit card companies, utility providers, and loan servicers have programmes for customers experiencing financial hardship. These often include temporarily reduced payments, lower interest rates, or deferred payments. A single phone call to your credit card company requesting a rate reduction costs nothing and succeeds more often than most people expect.

Step 6 — Free Up Cash Through Budget Optimisation and Income Growth

Getting out of debt faster requires either spending less, earning more, or both simultaneously. Both levers deserve active, deliberate attention throughout your payoff journey.

A budget tracks your monthly income against your outgoing expenses. Creating one helps you pay debt off faster by identifying ways to reduce spending and allocate more funds toward repayment.

On the spending side, the most impactful budget optimisations are the ones that reduce fixed monthly costs — because fixed cost reductions compound across every remaining month of your payoff journey. Call your service providers — internet, phone, insurance — and negotiate lower rates. A 15-minute phone call can save you $20-50 per month, which adds up to $240-600 per year toward debt payoff.

This means making a firm and genuine commitment to stop using credit for day-to-day purchases while you are in active debt payoff mode. It means removing your saved card details from online shopping platforms where impulse spending is just one click away. It means leaving credit cards at home when you go out and relying on what you actually have rather than what you can borrow.

On the income side, you could take on a side hustle. Driving for a ride-sharing service might be an easy way to make some extra cash. You can also consider freelancing or consulting within your industry, monetising a hobby, tutoring, starting a blog, or opening an online shop.

The average tax refund in 2026 is around $3,000. Putting that toward your highest-interest debt can save you hundreds in interest charges. Windfalls — tax refunds, bonuses, inheritance, gifts — should be directed immediately toward debt rather than spent. Every lump-sum extra payment reduces your principal and the interest that compounds on it from that day forward.

Financial Planning Insight: A certified financial planner can review your complete budget picture and identify the specific cost reduction and income optimisation opportunities that are most achievable given your specific income, lifestyle, and debt profile — turning a generic “spend less” directive into a specific, actionable monthly cash flow plan.

Step 7 — Use the Priority Framework for Every Extra Dollar

Every extra dollar available beyond minimum payments deserves deliberate prioritisation. Going through a “financial priority list” for extra income makes sense: “Contribute to your emergency fund,” first. If you already have three to six months of living expenses tucked away, pay off credit card debt and then “contribute more to your retirement accounts.”

The specific priority framework that produces the optimal financial planning outcomes in 2026 is:

Priority 1 — Employer 401(k) match. If your employer matches 401(k) contributions — even partially — contribute enough to capture the full match before directing extra dollars toward debt. An employer who matches 50% of your first 6% of salary contributions is giving you an immediate 50% guaranteed return on that contribution — better than the guaranteed return of eliminating even a 22% credit card.

Priority 2 — Eliminate high-interest debt. All debt above approximately 7-8% interest rate should be eliminated before investing further. The guaranteed return of eliminating 22% credit card debt exceeds any realistic investment management return expectation.

Priority 3 — Build full emergency fund. Expand your $1,000 starter emergency fund to three to six months of essential expenses once high-interest debt is eliminated.

Priority 4 — Invest aggressively. Once high-interest debt is gone and your emergency fund is fully funded, direct every available dollar toward investment management — maximising 401(k) contributions, funding a Roth IRA, and building a taxable investment portfolio.

Priority 5 — Pay down low-interest debt strategically. Mortgages, low-interest student loans, and other debt below 5-6% may be worth maintaining while investing simultaneously — particularly if your investment management strategy is generating consistent returns above the debt interest rate.

Step 8 — Build Accountability Into Your System

Find accountability. One idea is to look for an accountability partner, or someone you can share your goals and progress with. If they’re working toward their own financial goals, you could offer each other support. There are also accountability apps that can help you find motivation. Getting a professional’s perspective on how to approach your debt payoff goals can help you feel more confident that you’re on the right track.

“Getting a professional involved in your situation is not always necessary for debt payoff, but there can be benefits,” says Ashley Morgan. “If you need someone to keep you accountable or to review your finances, a financial advisor can be helpful. Sometimes I see clients that are unsure where they can realistically cut from their budget, so a second set of eyes never hurts.”

Automation is one of the most powerful accountability tools available. Set up automatic payments for all your debts to ensure you never miss a due date. This protects your credit score and avoids late fees. Automating your extra debt payment — the amount above minimums that drives your payoff strategy — means it happens before you have the opportunity to redirect that money elsewhere.

Keep updating your debt list periodically and at key moments, like when you pay off an account. Tracking your progress visually — whether through a debt tracking app, a spreadsheet, or a physical chart — provides the psychological reinforcement that sustains motivation across a payoff journey that may span months or years.

The Transition — From Debt Freedom to Wealth Building

The moment you make your final debt payment on that last high-interest account is one of the most significant financial moments of your life. But it is genuinely not the destination — it is the starting line.

Whatever route you take to tackle debt in 2026, make sure you’re reevaluating your relationship with spending. “Be very mindful of how much you owe. What are your monthly bills? Are they staying the same or going up? Things cost more, and your balance can shoot up without you really noticing.”

The habits that got you out of debt — disciplined spending, consistent extra payments, income optimisation, delayed gratification — are the same habits that will build your wealth management outcomes over the decades that follow. The difference is that after debt freedom, the extra monthly cash flow that was going toward debt payments can now go toward building wealth instead.

The practical transition looks like this:

Month 1 after debt freedom: Redirect every former debt payment dollar into maximising your 401(k) and opening a Roth IRA. The habit of directing that money is already built — you are simply changing its destination from debt elimination to investment management.

Month 3-6: Build your emergency fund to its full three to six month target — now that you no longer need the minimal $1,000 starter version.

Year 1 onward: Begin building your comprehensive financial planning framework — coordinating investment management, tax planning, retirement planning, and wealth management under one expert-guided advisory relationship that ensures every dollar works as hard as possible for your long-term financial security.

While you’re paying down debt, you can keep some money in low-risk investments to continue growing your wealth over time. For debt below 6%, simultaneous modest investing — particularly into employer-matched retirement accounts — makes mathematical sense. The wealth-building habit is worth establishing even while the final low-interest debt is still being paid down.

What Your Financial Life Looks Like After Debt — The Numbers

The most powerful motivational tool available during a long debt payoff journey is a clear, vivid picture of what your financial life looks like on the other side. Here are the real numbers that make the journey worth every sacrifice.

The average American with $104,755 in non-mortgage debt — making minimum payments on most of it — is directing approximately $1,500-$2,000 per month toward debt service. After aggressive payoff — even over three to five years — that $1,500-$2,000 per month becomes available for investment management.

$1,500 per month invested in a diversified portfolio at a historically reasonable 8% annual return grows to:

- $108,000 in 5 years

- $270,000 in 10 years

- $690,000 in 20 years

- $1.08 million in 25 years

The same debt payment that was building someone else’s wealth — your credit card company’s — becomes the investment that builds yours. The mathematics of compound growth, working in your favour rather than against you, is genuinely transformational across any meaningful time horizon.

How Synergistic Financial Advisors Helps You Bridge the Gap

At Synergistic Financial Advisors, we understand that the journey from debt to genuine wealth management is not a single decision — it is a coordinated financial strategy that evolves across multiple phases of your financial life.

Our certified financial planner team works with individuals at every stage of that journey — from building the initial debt payoff plan and optimising the priority framework for every extra dollar, to designing the investment management strategy that deploys freed-up cash flow for maximum long-term compounding, building the retirement planning framework that ensures debt freedom translates into genuine retirement security, and coordinating the tax planning strategy that ensures every investment is held in the most tax-efficient account structure from the beginning.

Your advisor can help you prioritise your debt and build in accountability so you’re able to get rid of bad debt. That way, you can put the money you were using to pay off debt toward more fun savings goals.

The transition from debt payoff to wealth management is the most financially consequential pivot in most people’s financial lives. Getting it right — with the right strategy, the right account structure, and the right professional guidance — creates compounding advantages that accumulate across every year of the wealth management journey that follows.

Ready to build your personalised path from debt freedom to genuine wealth? Contact Synergistic Financial Advisors today for a consultation built entirely around your specific situation.

👉 Visit www.sfaresearch.com — because getting out of debt is the beginning. What you build after is the point.

Final Thoughts — The Starting Line Is Closer Than You Think

Getting out of debt can help you reduce stress, free up funds and improve your financial life overall. While making only minimum payments keeps you in debt longer and can mean paying more in interest, being more aggressive in your payoff strategy could help you reach your goals more quickly.

Becoming debt-free doesn’t happen overnight, but it’s absolutely possible with a focused, realistic approach. The eight steps in this guide — understanding your debt, completing your inventory, building your starter emergency fund, choosing your payoff strategy, attacking credit cards with urgency, optimising your budget and income, applying the priority framework, and building accountability into your system — give you everything you need to begin today, regardless of where you are starting from.

The debt is real. The payoff journey is genuinely achievable. And the wealth management outcomes on the other side of that journey are more powerful than most people who are currently in debt can fully imagine.

At Synergistic Financial Advisors, we have guided individuals through exactly this journey — from the honest debt inventory conversation to the first investment management account opened with freed-up cash flow to the retirement planning strategy built on the foundation of genuine financial freedom.

The starting line is closer than you think. Let’s get you there.