The world is on the brink of the largest transfer of wealth in human history — and most families are not ready for it.

Approximately $124 trillion in wealth will change hands through 2048, with $105 trillion flowing directly to heirs and $18 trillion going to charitable organisations. Nearly $100 trillion — representing 81% of all transfers — will come from Baby Boomers and older generations as they pass their accumulated wealth to younger generations. This massive shift is already underway, with approximately $1.5 trillion to $2 trillion being transferred annually.

These numbers are extraordinary. But they are accompanied by a statistic that should concern every family building wealth in 2026: studies consistently show that 70% of family wealth is lost by the second generation, and 90% by the third. The reasons are rarely taxation, market performance, or bad investments. They are inadequate preparation of heirs, absent family governance structures, poor communication across generations, and the absence of a coordinated plan that treats wealth management as an ongoing, evolving system rather than a one-time inheritance event.

Preserving wealth is a continuous process, not a single event. Research consistently shows that families who sustain wealth treat planning as an evolving system that integrates investments, governance, education, and tax efficiency rather than relying solely on traditional inheritance mechanics.

In 2026, with the federal estate tax exemption permanently established at $15 million per individual, new legislative certainty around gifting rules, and an unprecedented volume of intergenerational wealth transfer underway, the opportunity to build a genuinely lasting multi-generational financial legacy has never been greater — and the cost of failing to plan has never been higher.

This guide gives you the complete 2026 framework for protecting family wealth management across generations — covering legal structures, tax planning strategies, governance frameworks, financial education, and the coordinated advisory approach that ties everything together.

Why 70% of Family Wealth Disappears by the Second Generation

Before examining the strategies for protecting wealth across generations, it is essential to understand why family wealth so consistently fails to survive beyond the first or second generation — because the answer is not what most people expect.

The point is not just to transfer money — it is about preparing those who will inherit it. Studies on generational wealth consistently show that financial capital alone does not sustain legacy.

The primary causes of multi-generational wealth erosion are not market crashes or taxation. They are the absence of financial literacy among heirs, poor communication between generations about money and family values, inadequate governance structures for shared family assets, lack of preparation for the psychological and practical responsibilities of inherited wealth, and family conflict that emerges when expectations are not clearly communicated in advance.

Wealthy families in 2026 are approaching generational wealth differently than previous generations. The focus is shifting from pure asset preservation toward long-term family continuity. The families most likely to preserve wealth successfully are those that communicate intentionally, prepare future generations, simplify complexity, coordinate planning thoughtfully, and remain adaptable over time.

This insight is the foundation of modern generational wealth management: protecting family wealth across generations is not primarily a legal or financial challenge. It is a human challenge — one that requires deliberate attention to communication, education, governance, and family culture alongside the legal structures and tax planning strategies that most traditional estate planning focuses on exclusively.

Strategy 1 — Build a Comprehensive Estate Plan as the Legal Foundation

A comprehensive estate plan is essential for the orderly transfer of wealth. The purpose of an estate plan is to give you control over how your assets are distributed while minimising the effects of estate and gift taxes. Employing a combination of strategies will support your wealth goals and protect your family’s legacy.

The foundational legal structure for protecting family wealth across generations begins with a comprehensive estate plan — one that goes significantly beyond a basic will to incorporate trusts, beneficiary designations, powers of attorney, and specific provisions designed for multi-generational wealth transfer.

Estate planning is the process of establishing legal documents that direct how your assets should be managed and distributed following your death. A thoughtful estate plan also addresses who will make financial and healthcare decisions on your behalf if you become incapacitated.

For families with meaningful wealth to protect and transfer, this foundational estate plan should incorporate trusts as the primary structure — providing probate avoidance, privacy, ongoing distribution control, incapacity management, and asset protection across multiple generations. Trusts serve as the primary mechanism for controlling how assets are distributed, helping protect them from creditors, divorce claims, or poor financial decisions. With thoughtful trust planning, you can also establish clear terms for how future generations receive their inheritance.

The estate plan also needs to coordinate with your investment accounts, beneficiary designations, insurance policies, and tax planning strategy — because the most costly estate planning failures almost always occur at the intersection of these elements rather than within any single document. Working with a financial advisor who coordinates with your estate planning attorney and CPA ensures this integration is complete and coherent.

Financial Planning Insight: A certified financial planner who reviews your complete asset inventory against your estate planning documents can identify specific gaps between your stated wishes and your actual account structure — ensuring that every asset reaches its intended beneficiary through the most appropriate, most tax-efficient, most privacy-protective vehicle available.

Strategy 2 — Maximise the 2026 Gifting Opportunity Before It Changes

The One Big Beautiful Bill Act permanently increased the federal estate and gift tax exclusion to $15 million per individual — $30 million for couples — beginning in 2026, providing significant certainty for estate planning. This legislation prevented the automatic decrease in the basic exclusion amount that would have occurred on January 1, 2026.

This is one of the most significant and most time-sensitive generational wealth management opportunities in recent legislative history. With the estate tax exemption now permanently at $15 million per individual, families have an unprecedented window to transfer wealth to the next generation without federal estate tax — and with the annual gift exclusion providing additional, immediate gifting capacity.

Individuals may transfer up to $15 million during their lifetime or at death without incurring any federal gift or estate taxes. In addition, individuals may gift up to $19,000 annually to any individual without incurring any federal gift tax liability or using the lifetime exemption.

For a married couple with two children and four grandchildren, the annual exclusion alone allows $228,000 per year in completely tax-free gifts — $38,000 per recipient per year — that simultaneously reduce the taxable estate and provide immediate financial benefit to the next generation.

Upstream gifting — making a gift to an older family member rather than directly to a younger family member — may allow the parent to take advantage of today’s high lifetime gifting exemption and the step-up in basis. When the grandparent passes away, the assets receive a step-up in cost basis, effectively erasing any gains that have occurred since they were originally acquired.

This upstream gifting strategy is one of the most sophisticated and most powerful generational wealth management tools available in 2026 — combining the lifetime exemption with the step-up in basis to eliminate both estate tax and capital gains tax on highly appreciated assets simultaneously.

Financial Planning Insight: Systematic annual gifting — implemented as a deliberate, year-round programme coordinated with your overall tax planning and wealth management strategy — creates compounding generational wealth management benefit that a single large transfer at death cannot replicate. A financial advisor can design the optimal gifting programme for your specific family structure and asset base.

Strategy 3 — Use Dynasty Trusts for Multi-Generational Wealth Preservation

For families seeking to protect wealth not just for children but across multiple generations — potentially indefinitely — dynasty trusts represent one of the most powerful tools available in 2026.

Dynasty trusts allow wealth to pass from generation to generation without incurring transfer taxes at each level. These can be set up as irrevocable trusts, which lock the assets away from your personal estate tax calculation.

A dynasty trust — established in a state with favourable trust law such as South Dakota, Nevada, or Delaware — can hold assets for multiple generations without the assets being subject to estate tax at each generational transfer. Under the generation-skipping transfer tax rules, proper planning with the available generation-skipping exemption — currently also $15 million per individual in 2026 — allows substantial assets to pass to grandchildren and great-grandchildren without estate tax at the intermediate generational level.

Trusts are not just about tax savings — they are also about fiduciary oversight. Families often structure a trust where the child has access to income at disparate ages — such as 25, 30, and 35 — to prevent heirs from dissipating an inheritance in their early twenties.

This controlled distribution structure is one of the most practically important features of trust planning for families concerned about heir preparation. An 18-year-old who inherits $2 million outright faces very different — and much more difficult — financial decisions than an heir who receives trust income at 25, a portion of principal at 30, and full access at 35. The phased approach provides genuine financial support while protecting the wealth from the poor decisions that statistically cluster in early adulthood.

Financial Planning Insight: Dynasty trust planning requires careful selection of trust jurisdiction, trustee structure, distribution standards, and trust protector provisions. A financial advisor coordinating with a trust attorney can model the multi-generational wealth preservation impact of different trust structures against your specific family circumstances and asset profile.

Strategy 4 — Implement Robust Asset Protection Structures

Protecting family wealth across generations is not only about preventing erosion through taxation — it is equally about protecting assets from creditors, divorce claims, lawsuits, and other external threats that can rapidly deplete inherited wealth.

Strategic property ownership for families planning to transfer real estate involves shared ownership structures in some situations. However, trust-based strategies are often preferred to transfer real estate while maintaining better tax protection.

The most effective asset protection structures for multi-generational wealth management include spendthrift trust provisions — which prevent beneficiaries from assigning their interest in the trust to creditors and prevent creditors from reaching trust assets before distribution. Family Limited Partnerships and Limited Liability Companies can consolidate family business and investment assets under a governance structure that provides both asset protection and valuation discounts for gift tax purposes.

Irrevocable trusts remove assets from the grantor’s estate entirely — protecting them from both estate tax and personal creditors. When properly structured, assets in an irrevocable trust are beyond the reach of a beneficiary’s creditors until the moment of distribution, providing genuine protection for family wealth across the full span of a trust’s duration.

Tax strategy continues to play a major role in generational wealth planning. Affluent families increasingly evaluate gifting strategies, trust structures, charitable planning, residency considerations, estate tax exposure, and business succession planning. As tax laws continue evolving, flexibility has become increasingly important.

Strategy 5 — Build Family Governance Structures

Many high-net-worth families now view wealth education as equally important as wealth transfer itself. This reflects a broader evolution in wealth management philosophy. The goal is no longer simply preserving assets — it is preparing future generations to navigate complexity thoughtfully.

Family governance is the dimension of multi-generational wealth management that most traditional estate planning completely ignores — and the one that research most consistently identifies as the primary determinant of whether family wealth survives beyond the second generation.

Families who successfully maintain wealth across generations often pair legal protections with governance practices such as investment policies, structured decision-making processes, and routine financial reviews. These practices help ensure everyone is on the same page and that assets remain aligned with both current needs and long-term goals.

Family governance structures for wealth management include regular family meetings where financial matters are discussed openly across generations, written investment policy statements that document the family’s investment philosophy and risk tolerance, family mission statements that articulate shared values and the purpose of family wealth, and formal decision-making processes for shared assets such as family businesses, vacation properties, and investment holdings.

Family governance establishes continuity frameworks that dictate how decisions are made regarding family businesses or vacation homes long after the original owners are gone.

The families that successfully pass wealth across generations are not those with the most sophisticated trust structures or the most aggressive tax planning strategies — they are those that have built genuine family communication and shared understanding around the purpose, management, and values associated with their wealth. That communication is what prevents the family conflict that most commonly triggers wealth erosion between generations.

Financial Planning Insight: A financial advisor who facilitates family meetings, helps develop investment policy statements, and provides the educational foundation that allows heirs to participate meaningfully in wealth management conversations is providing one of the most valuable and most underappreciated services in generational financial planning.

Strategy 6 — Financial Education for Every Generation

Perhaps the most fundamental strategy for preserving generational wealth is making sure each generation possesses the knowledge and skills to manage it effectively. Basic financial literacy education starting from a young age is the foundation of wealth preservation, helping ensure each generation has the knowledge and skills to manage assets effectively.

Financial education is the single most important non-legal, non-financial strategy for protecting family wealth across generations. The statistics on wealth erosion between generations are not caused by bad markets or poor investment choices — they are caused by heirs who lack the knowledge, the confidence, and the values to steward inherited wealth responsibly.

Financial literacy is the knowledge and understanding of key financial concepts such as budgeting, saving, and investing to make informed financial decisions. Understanding financial concepts is essential for making sound decisions about wealth, investments, and legacy. It nurtures a sense of stewardship rather than entitlement, helping the next generation preserve and continue the legacy created.

Effective financial education for the next generation is not a single conversation — it is a developmental programme that evolves as family members mature. For young children, this means basic concepts around earning, saving, and the value of money. For teenagers, it means understanding how investments work, what debt costs, and how compound growth creates wealth over time. For young adults, it means understanding the specific trust structures, estate plans, and investment management strategies that govern the family’s wealth — and developing the skills to participate in family financial decisions responsibly.

Active stewardship involves guiding heirs on how to manage the wealth, ensuring the assets become a blessing rather than an overwhelming burden.

The goal of financial education for heirs is not to produce professional investors or financial experts. It is to produce thoughtful, informed stewards of family wealth — people who understand the responsibility that comes with inherited assets and who have developed the values and skills to honour that responsibility across their own lifetimes.

Strategy 7 — Integrate Philanthropy into Your Generational Wealth Plan

Unlike previous generations, younger heirs are more likely to embrace giving while living, prioritising charitable giving, impact investing, and values-based wealth management as core components of their financial strategies.

Integrating philanthropy into your generational wealth management plan serves three distinct and mutually reinforcing purposes: it provides genuine tax planning benefits that reduce the transfer tax burden on inherited assets, it instils values of stewardship and responsibility in the next generation, and it creates a shared family purpose around wealth that transcends the purely financial.

A donor-advised fund is one of the most accessible and most flexible philanthropic vehicles for families — allowing immediate tax-deductible contributions funded by cash or appreciated securities, with distributions to chosen charities made over any timeline. A Charitable Remainder Trust provides income during the grantor’s lifetime while ultimately transferring remaining assets to a charitable beneficiary — providing both tax planning advantages and philanthropic legacy. A family foundation creates the most formal philanthropic governance structure — with a board, an investment policy, and a grant-making process that can actively involve multiple generations in shared charitable decision-making.

Integrating philanthropy into your wealth preservation strategy provides tax benefits and instils values that help future generations become responsible stewards of wealth.

The philanthropic dimension of generational wealth management is increasingly viewed by sophisticated families not as a separate charitable activity but as an integrated component of their multi-generational financial planning — one that simultaneously serves tax planning goals, heir education objectives, and the family’s legacy intentions.

Financial Planning Insight: A financial advisor who integrates charitable giving strategy with your overall wealth management plan — coordinating donor-advised fund timing, charitable remainder trust structuring, and family foundation governance — delivers genuine, coordinated value that charitable giving in isolation cannot replicate.

Strategy 8 — Plan for Business Succession

For families whose wealth is substantially concentrated in a business, succession planning is the single most complex and most consequential dimension of multi-generational wealth management — and the one most likely to either protect or destroy family wealth in a single transition.

Business succession planning increasingly sits at the centre of modern generational wealth strategies. Without preparation, business transitions can create family conflict, operational instability, tax inefficiencies, and liquidity stress.

Effective business succession planning addresses four distinct challenges simultaneously. Ownership transfer — determining how business equity passes to the next generation or to outside buyers, through gift, sale, or trust, in a manner that is both tax-efficient and fair to all family members. Management succession — identifying, developing, and transitioning the operational leadership of the business to capable successors, whether family members or professional management. Liquidity planning — ensuring that family members who inherit business interests but do not work in the business can access appropriate liquidity without forcing the sale of operating assets. Valuation strategy — managing the timing and structure of business transfers to optimise the valuation for both gift tax and business succession purposes.

This requires a shift in mindset from simply hoarding assets to actively managing how those assets flow to the next generation, establishing continuity frameworks that dictate how decisions are made regarding family businesses long after the original owners are gone.

A family business that transfers successfully to the second generation — with clear governance, capable leadership, appropriate liquidity, and aligned family expectations — is one of the most powerful generators of sustained multi-generational family wealth. A business that transfers poorly is one of the most common sources of catastrophic wealth erosion.

Strategy 9 — Coordinate Your Digital Asset Estate Plan

In 2026, the unfunded trust problem is even more complex because so much of what we own is digital and does not have a paper deed. Digital assets — like online accounts, loyalty points, or cryptocurrency — are often left out of trusts. If your successor trustee does not have a map to these assets and the passwords to reach them, the assets may be lost forever.

Digital assets represent a genuinely new and genuinely significant dimension of multi-generational wealth management — one that most estate plans drafted before 2020 completely fail to address. In 2026, digital assets can include cryptocurrency holdings worth significant sums, digital business assets such as websites and intellectual property, online brokerage and banking accounts, loyalty programmes with accumulated value, and digital media collections.

The Revised Uniform Fiduciary Access to Digital Assets Act has been enacted in 47 states as of early 2026. This law provides the legal framework for your executor to manage your digital life, but it only works if you have explicitly granted that permission in your legal documents.

Protecting digital assets across generations requires three specific actions: explicit authorisation within your legal documents for your executor or successor trustee to access digital accounts, a secure documented inventory of all digital assets and their access credentials, and regular updating of this inventory as new digital accounts are created or existing ones change.

Strategy 10 — Simplify and Coordinate Your Wealth System

Many affluent families are now prioritising simplification alongside sophistication. Over time, financial systems can become highly fragmented through multiple trusts, scattered accounts, overlapping advisors, and outdated structures. In response, many families are working with wealth management advisors to improve visibility, coordination, organisation, and operational continuity.

This is one of the most practically important and most consistently underappreciated dimensions of multi-generational wealth management. Complex, fragmented financial systems — with accounts at multiple institutions, advisors who do not communicate with each other, outdated trust structures, and unclear asset inventories — are genuinely dangerous to family wealth preservation. They create gaps that the wrong assets slip through, inefficiencies that compound across decades, and confusion that generates family conflict at exactly the moments when clarity is most needed.

The best multi-generational wealth management systems are not necessarily the most sophisticated ones — they are the most comprehensively coordinated ones. A single, integrated advisory team that can see the complete picture across legal structures, investment accounts, tax planning, estate planning, philanthropy, and heir education is more valuable than a collection of separate specialists who each optimise their individual dimension without awareness of how it affects the whole.

Holistic wealth management begins by implementing long-term investment strategies designed for longer-term time horizons, allowing growth to compound over decades. It also takes a coordinated effort with outside advisors such as an estate planning attorney and accountant to curate an individualised plan to ensure those goals are met.

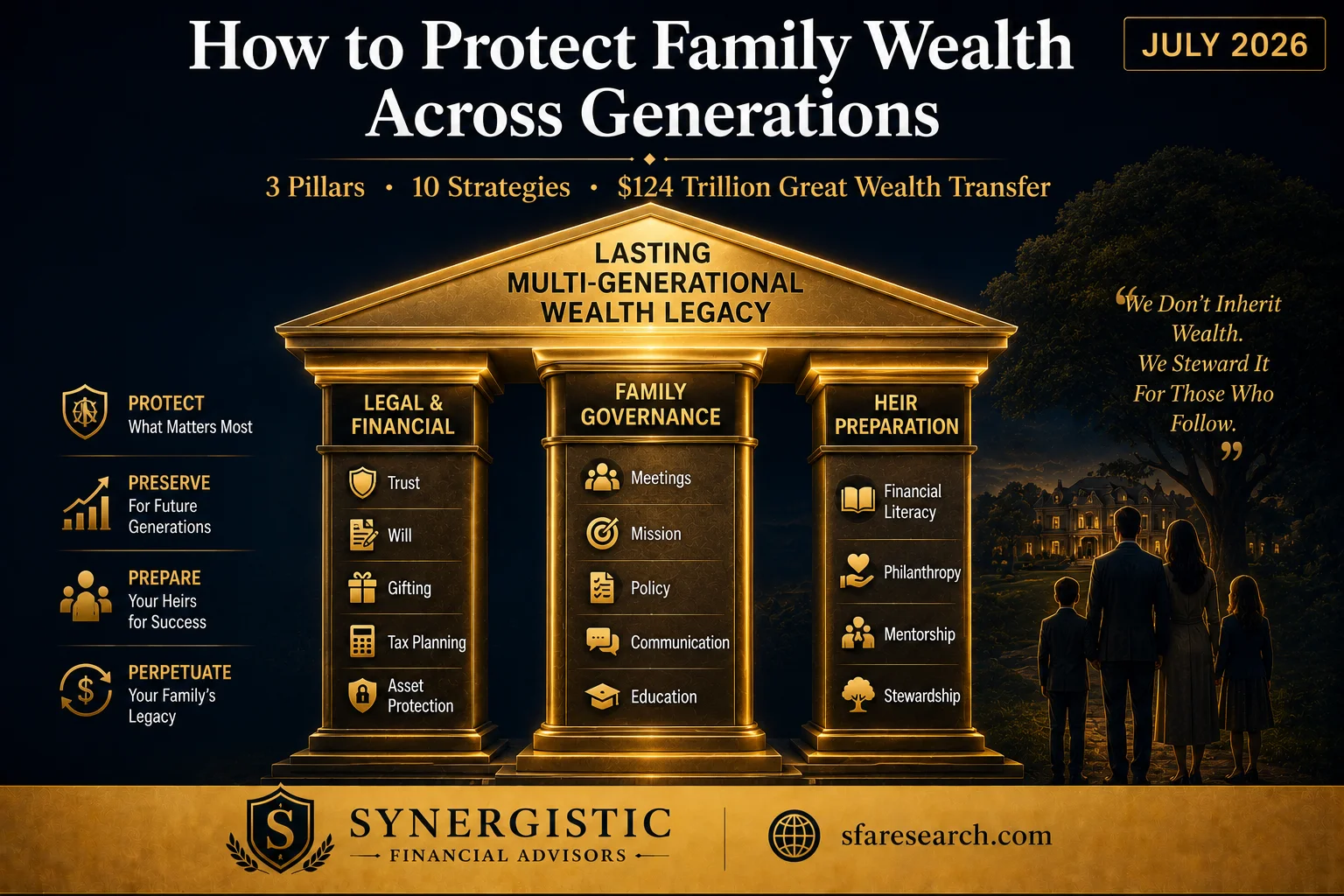

The 3 Pillars of Lasting Multi-Generational Wealth

Synthesising everything above, the research consistently identifies three pillars that distinguish families who successfully protect wealth across generations from those who do not.

Pillar 1 — Legal and Financial Infrastructure. Comprehensive estate planning, appropriate trust structures, systematic gifting programmes, tax planning integration, asset protection structures, business succession planning, and coordinated beneficiary designations — all working together as an integrated system rather than a collection of separate documents.

Pillar 2 — Family Governance and Communication. Regular family meetings, investment policy statements, family mission documents, clear decision-making processes for shared assets, and transparent communication across generations about the family’s financial situation, values, and expectations.

Pillar 3 — Education and Heir Preparation. Developmental financial literacy programmes that evolve as family members mature, deliberate exposure to financial planning and investment management concepts before inheritance occurs, philanthropic engagement that builds stewardship values, and active mentorship from the wealth-creating generation to the wealth-inheriting generation.

At the end of the day, trust, communication, and structure help turn wealth into a long-term plan rather than a collection of investments.

How Synergistic Financial Advisors Protects Your Family’s Wealth Across Generations

At Synergistic Financial Advisors, we understand that protecting family wealth across generations is the most complex and most consequential dimension of financial planning — one that requires expertise across investment management, tax planning, estate coordination, family governance, heir education, and philanthropic strategy, all working together under one integrated advisory relationship.

Our certified financial planner team works with families at every stage of the generational wealth journey — from building the foundational estate plan and implementing systematic gifting programmes, to designing trust structures for ongoing distribution control, coordinating business succession planning, facilitating family governance conversations, and developing the heir education programmes that prepare the next generation to steward inherited wealth responsibly.

We coordinate directly with your estate planning attorney and CPA — because the most powerful generational wealth management happens when legal, financial, and tax professionals are working from the same coordinated plan with full visibility into the complete family picture.

Ready to build a plan that protects your family’s wealth not just for your lifetime but for the generations that follow? Contact Synergistic Financial Advisors today for a personalised generational wealth management consultation.

👉 Visit www.sfaresearch.com — because the greatest gift you can leave your family is not just wealth but the plan that protects it.

Final Thoughts — Legacy Is Built With Intention, Not Luck

The $124 trillion Great Wealth Transfer underway in 2026 will not automatically produce lasting family legacies. It will produce lasting legacies for the families who plan intentionally — who build the legal structures, the governance frameworks, the educational programmes, and the coordinated advisory relationships that give wealth a genuine chance of surviving the transition from one generation to the next.

Preserving wealth across generations is not simply about protecting assets. It is about protecting clarity, alignment, and stewardship alongside them.

At Synergistic Financial Advisors, protecting your family’s wealth management legacy — across every generation you intend to serve — is the most meaningful work we do.